Hi to everyone.

After the

last post with allocations, I'm going with

more details about 2015 and changes for 2016.

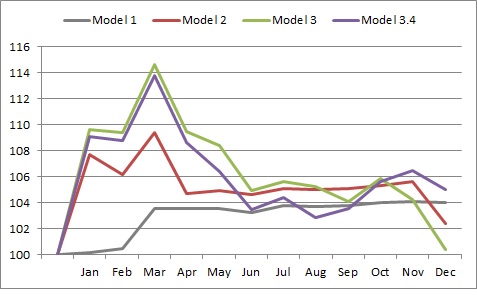

First of all you can see the performance of the allocations on the Etfs's benchmark on monthly basis. I don't consider transactions costs, taxes and slippage, therefore is just for example. In real performance would have been different of course, but the trend is this.

Knowing the future the optimal choice would have been to take money out in march and go in holiday for the rest of the year :)

The first thing that appear in the graph is that

models began 2015 really strong, then the trend with severa months of life reverted and began a choppy period. My models suffered the second part of the year, especially the model 3 original.

A positive thing is that all models finished the year with a plus on theorical basis.

The

Model 4 € close the year with a +2,8% return vs 5,3% of the equal weighted benchmark. It lagged the benchmark because of low exposure on european equity.

On the other side of Atlantic,

Model 4 $ overperformed the equal weighted benchmark +0.4% vs -2.3%, therefore it did its job.

As you can check in the

last post about January Allocations, I posted more variations of the models.

Aggressive and with changing weights.

I did it for

3 motives:

1) First, I made many months of out of sample test without posting on the blog and they performed in line and/or better that the original one;

2) the market conditions in 2016 could lead to some change of strategies

3) they could be more convenient for some kind of investor with higher risk profile

A

big problem for me (and not only) is the negative interest rates on the safer shorter government bonds in Europe. This will lead to have a sure loss when I go defensive. On the other side e

quity markets are not cheaper anymore therefore I don't feel comfortable with very aggressive models. I believe that in coming years returns of main assets will be lower than average last 3-4 years, therefore it could become more important to save money (and avoid deep losses) that look for high returns.

On the other side cash gives negative returns (or almost zero if you are a retail), therefore one must do something.

I am going to do that

1) I'll

stick with defensive models 1 and 2, knowing that especially the 1 could lose next year.

2) I fear that

models will experience higher volatility than historical, therefore I'll reduce money invested on them and I'll raise discretional choice;

3)

I'll try to take some returns increasing that risk on model 3 using the aggressive variation. These means that the new versions of old models will try to raise equity exposure being in/out more often.

4)

I don't use the model 4 for myself as my capital isn't high enough for that diversification and taxes, fees will kill my returns. I don't use model 3 with changing weights every months because the same reasons.

I fear that

2016 won't be rich, but as I can't know how the year will be in real (I can forecast but without the crystal ball), I'll diversify my discretionary investments with these models, trying to get some positive returns.

I believe

volatility will be high these year and could not be for trend following models, but let's surf the sea again. The worst thing is a choppy year without trends on main assets...or an year where bond and stocks go down together.

Good luck to everyone!!! Central banks excesses could show collateral effects starting this year

PS. The model I'll try to check this year will be these. They are many and this raise the chance of mistakes when I post returns and write allocations. To minimize this risk I'll try to post allocations at the beginning of each month as soon as I can, and post the considerations/performance over the month when I have time. In red the new version. Below correlations since 2000 where you can see that some are low correlated, other aren't. Being all trend follower methods, correlations are positive.

MODEL 1

MODEL 2

MODEL 3 -

MODEL 3 (more aggressive) ***

MODEL 3 Variable weights ***

MODEL 3.4

MODEL 3.4 Variable weights ***

MODEL 3.4 (more aggressive) ***

MODEL 3.5 ***

MODEL 4 €

MODEL 4 € equity push

MODEL 4 USA

MODEL 4 USA equity push