Note: I updated this post because I found a bug in the return calculation while building this same model with US ETF. Basically the return was wrong for €bonds 1-3years as I took another asset. With correct benchmark, the risk/return parameters improve, validating the strength of model.

In this post I want to show a model I developed that is different from the previous I posted.

While model 1, 2 and 3 were absolute returns models, ie trying to close basically positive in the long term, reducing downside risk,

MODEL4 try to beat a benchmark with a better risk/return

BENCHMARK

I suppose that my universe is composed by

9 assets that can be a proxy of major asset classes for an European investor. I replicate them with ETFs.

CASH: as

proxy I use Ishares € government 1-3 years because negative rates (in real as retail you can also use a sight deposit with positive/zero rate)

BOND:

- ishares Core euro government bond (proxy for € govies)

- ishares JP Morgan $ emerging markets (proxy for emerging market bonds)

- Ishares € high yield corporate bond (proxy for euro high yield bonds)

- Ishares global government bond (proxy global bond market)

EQUITY

- ishares MSCI EMU (proxy for euro equity)

- ishares MSCI World (proxy for world equity)

ALTERNATIVE

- Ishares developed markets property yield (proxy real estate)

- Bloomberg commodity index euro (proxy for commodity and benchmark for some Etf)

My benchmark is the equal weight portfolio (EW portfolio) with monthly rebalance (ie Etf has 11,11% weight)

MODEL vs BENCHMARK

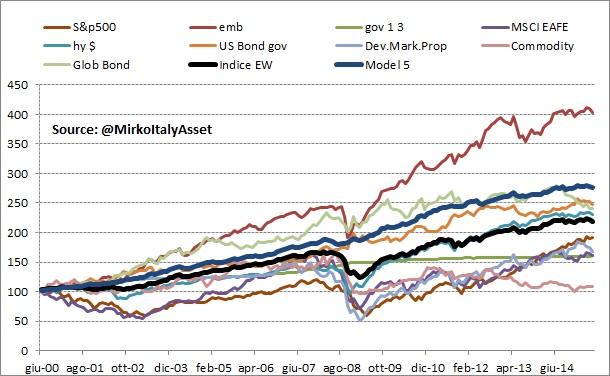

MODEL 4 is able to beat benchmark over long term mostly by reducing draw-down in difficult environments.

Below you can see the graph where the MODEL (dark blue) outperforms the EW portfolio (black line). You can see also the returns of others asset classes in the same period of time.

The table below confirms the outperformance.

MODEL 4 returns approx only 1% a year more than benchmark over the long term, but the huge difference is the draw-down and the volatility. MODEL 4 contain the max DD at less than 3%, while EW portfolio lost more than 27% once. You slept definitively better with the model even if returns are not much higher. And in the long term MODEL 4 (but also the EW portfolio) outperformed the risk free rate (Eonia).

PRO & CONS

I want to show a quality (and a defect) of the model. In the chart below you can see the ratio MODEL 4/EW portfolio. Basically when line rise the MODEL outperforms the benchmark and vice versa. You can see that

there's a strong outperformance when there were stress on markets as 2007/08 and 2001/02. Instead when the market is in strong "risk on" phase, the MODEL tends to underperform from a simple return point of view.

This is a quality that I appreciate because

it's "natural" and not overfitted.

My goal is always to find models that can continue to work in the future with high probability, therefore I believe that is important to not overfit. I have a clear trading concept, I put on place and don't go to see if modifying one parameters it improves. What I do is to have the idea and see if, changing parameters, the idea works with stable results.

If it doesn't work, it goes in the garbage. For example, I dont' use in this model moving averag, but just to explain the concept: if it works with 60days, doesn't with 100days, works with 120 and works so so with 200, for me it goes in the garbage :)

CONCLUSION

MODEL 4 in the past was able to outperform an Equal-weighted portfolio with 9 asset classes from an European investor side.

Returns were not a lot superior, but the biggest difference is the more conservative approach that avoid the drawdown. I accept the underperform in the "risk on" situation because I know that with an high probability MODEL will outperform in long term with much lower draw dawn that help me to sleep better.

Just to be fair: Year to date the model underperforms the EW portfolio.

At the end of June EW returns7,2%, while MODEL 4 returns just +1.6%. Therefore it shows that is not overfitted otherwise I would have posted a better result :)

Allocation for JULY: 100% euro government 1-3 years. Very defensive. Don't know how Greek situation will evolve, maybe I'll lose a relieve rally, but I sleep very well :)

I'll update it with the other montlhly allocation post every month in this 2015.

{kind=link}

{kind=link}

{kind=link}

{kind=link}