Disclaimer: In this post I write my opinions and trading idea. If you choose to act like me, you are assuming your responsibility for your investment decision, because I could be wrong as every human being.

Good morning everybody,

this week was quite volatile thanks to the unexpected (not for me, my office colleagues are witnesses :) ) Trump's victory.

What surprised me was the market reaction. I believed that Trump was more equity friendly than Clinton, but I was quite confident that the initial reaction (at least for 1-2 weeks) would have been negative.

My idea was a sort of pretty decent fall at the beginning, the break of 2000 level on S&P500, long short term traders washout, choppy markets for some weeks and new highs in 2017.

I was wrong on that, the fall lasted only few hours.

With this post I want to point out some variables to monitor in the following weeks, expected to be volatile after the initial exuberance. I want to see it from a

weekly chart point of view. It's a time period that I appreciate a lot and, according my experience, personal goals and character, is more adapt to realize what is going on. I also like monthly charts, while I don't like daily on indexes because of algos that can fake them easier

S&P500

Days ago I posted a similar chart on Twitter. I pointed out the risk of a Sma10-EMA20-30 weekly cross on the S&P500 in the next few weeks. In the last 2 times it happened, volatility increased sharply after the cross.

I want to point out few things:

- Every bear market began with this bear cross, but not every cross leads to a bear market (so don't scream when it happens, just be alert).

- In the last 2 events (Summer 2015 and beginning 2016) the cross came just close to the market bottom. But in the following 4 weeks market was very choppy

- Note above how the white weekly candle of this week could remind the one of July 2015. The environment is not exactly the same for the index (S&P500 was flat at that time, while at the moment market is decreasing since August and S&P rose above a short term resistance. The environment is pretty similar for the moving averages shape.

SUMMARY: this positive week reduced the fear of a moving average cross in the next 1-2 weeks, but be careful that in a time frame longer than daily, technical situation continues to show weaking. Personally, I won't yell out "Beware to be long, the bear is out" because

long-term trend is still up. I continue to think that, if market will fall sharply before end of year, it's still a buy opportunity when Vix rise around 28-30%

GOVERNMENT BONDS

This is the ETF Ishares Core US Treasury Bond, a proxy for the Treasury market. As we can see, the sell off was very sharp, but i

t is approaching a support area . Volatility could continue, but I believe that, at the moment is quite likely that the

ETF will rebound at the first touch. I'd buy around

24.50 if touched to sell 0.80-1$ above on the rebound

GOLD

Gold is going to have a

moving average bear cross. The question is...w

ill it be like in 2013 or will be similar to the last few years,where gold was quite choppy after the cross? I think it's not yet ready to crash like in 2013. First the area between 1200-1150$ has many supports, second Gold suffered the fast rise in Governmente bonds interest rates and, as I said above, a rebound is likely short term. Important: the

ETF gold amount is still rising, meaning that institutional investor are buying and the sell of is probably linked to future action (speculator?) I think G

old will go choppy in the coming weeks. I'd be a buyer if drops around

1150$ (Disclaimer: I've already have a long term structural Gold position).

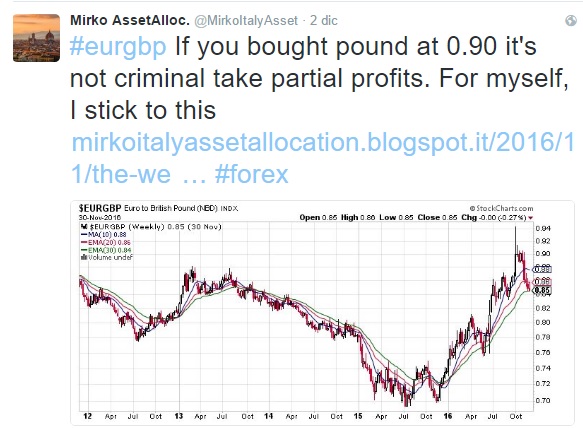

EUR/GBP

Let's return to the

Brexit theme. Brexit had a temporary stop with the High UK Court decision. Now the word passes in January (probably) to the Supreme Court. In UK the chances of earlier elections increased, but the situation is quite random. Probably, neither the Premier Theresa May nor MPs know how they will act in 2017. I continue to

buy sterling on weaknesses (I bought shy above 0,85 and above 0,90) but

I'll wait the Supreme Court decision for the next purchases.

Technically uptrend is still strong and between 0,87 and 0,83 there's a strong support area. I'd be careful buying sterling further at this level after this strong week. Better buying on weakness.

I'd continue to be a seller of all Sterling, before Supreme Court decision, if Eur/Gbp fall towards 0,80 area. I could reduce exposure at 0,83.

{kind=link}